Here's the Property Trap Investors Are Walking Into

Every second call I've taken at Baker Advocates since the May 2026 Federal Budget is a variation of the same question: "Should I rush a new build to lock in negative gearing before it disappears?"

The short answer is no, and the data explains why with brutal clarity.

The May 2026 Budget introduced the most significant changes to Australian property tax policy in nearly three decades. From 1 July 2027, negative gearing on established residential properties purchased after 7:30pm on 12 May 2026 will be limited. Losses from those investments will only be able to be offset against rental income or future capital gains — not against personal salary, as has been the case for the last 40 years.

New builds are exempt. Existing property holdings are grandfathered. Which has created an almost immediate wave of "buy new to lock in the deduction" marketing across the country.

The problem: the exact type of stock that still qualifies new builds in outer growth corridors is also the type of stock the data shows as most overheated right now. The tax lever is pushing investor money into precisely the wrong markets, at precisely the wrong point in the cycle.

Here's what the numbers say.

What Actually Changed on Budget Night

A quick recap so this article works whether you're reading it fresh or as a refresher.

The cutoff. Any established residential property purchased after 7:30pm on 12 May 2026 loses access to negative gearing from 1 July 2027 onwards. Between now and 1 July 2027, negative gearing on those post-cutoff purchases still applies. After that date, rental losses can only be offset against rental income or future capital gains from investment property.

The exemptions. New builds (eligible new residential dwellings) remain fully negatively-gearable and still access the 50% capital gains tax discount. Properties owned before 7:30pm on 12 May 2026 are grandfathered and continue to be treated under the old rules until sold. Properties held via widely-held trusts and superannuation are exempt.

The window. Investors have roughly 12 months (until 30 June 2027) before the changes bite on post-Budget established purchases. From 1 July 2027 onwards, only new builds preserve the full tax structure indefinitely.

That last point is what's driving the market behaviour we're seeing right now.

Why New Builds Are Suddenly the "Safe" Story

The tax logic is straightforward: if the goal is to preserve negative gearing indefinitely as it was previously in place, new builds are the only remaining path.

The unstated assumption the one causing damage is that "preserving negative gearing" is a good enough reason to make the purchase decision. It ineve has been and it never will be for most. Tax benefits such as negative gearing were never the goal. Captial growth and creating wealth were.

The type of stock most often marketed as "eligible new build" is stock in outer growth corridors house-and-land packages in new estates, on the fringe of Sydney, Melbourne, Perth, and Brisbane. Those are exactly the markets where the underlying capital growth story matters most, because you're relying on land price appreciation to overcome the meaningful premium new-build stock carries over comparable established houses in the same area.

And those are exactly the markets where the data says the growth story is furthest through its run.

The Data on Where the Panic Money Is Going

I ran three archetypal "eligible new-build" suburbs this month, one from each of the states most-targeted by new-estate marketing:

Marsden Park — north-west Sydney growth corridor

Baldivis — south-west Perth outer suburb

Kingston — Brisbane's southern corridor (Logan LGA)

All three sit at the "(+)Decreasing" phase of the growth-rate cycle meaning their growth rate is now cooling from an already-hot base. Each has posted strong 12-month and 5-year returns. Each is being pitched to investors right now as a negative-gearing-safe purchase.

The critical metric to look at underneath the headline growth is Growth Pattern Deviation (GPD), this is how far a suburb's current price sits above or below its own long-term trend line. Positive GPD means the suburb has run ahead of its own history. Negative GPD means it's lagged. In simple terms: GPD tells you how much of the future growth has already been pulled forward into current pricing.

Here's how the three suburbs look on GPD.

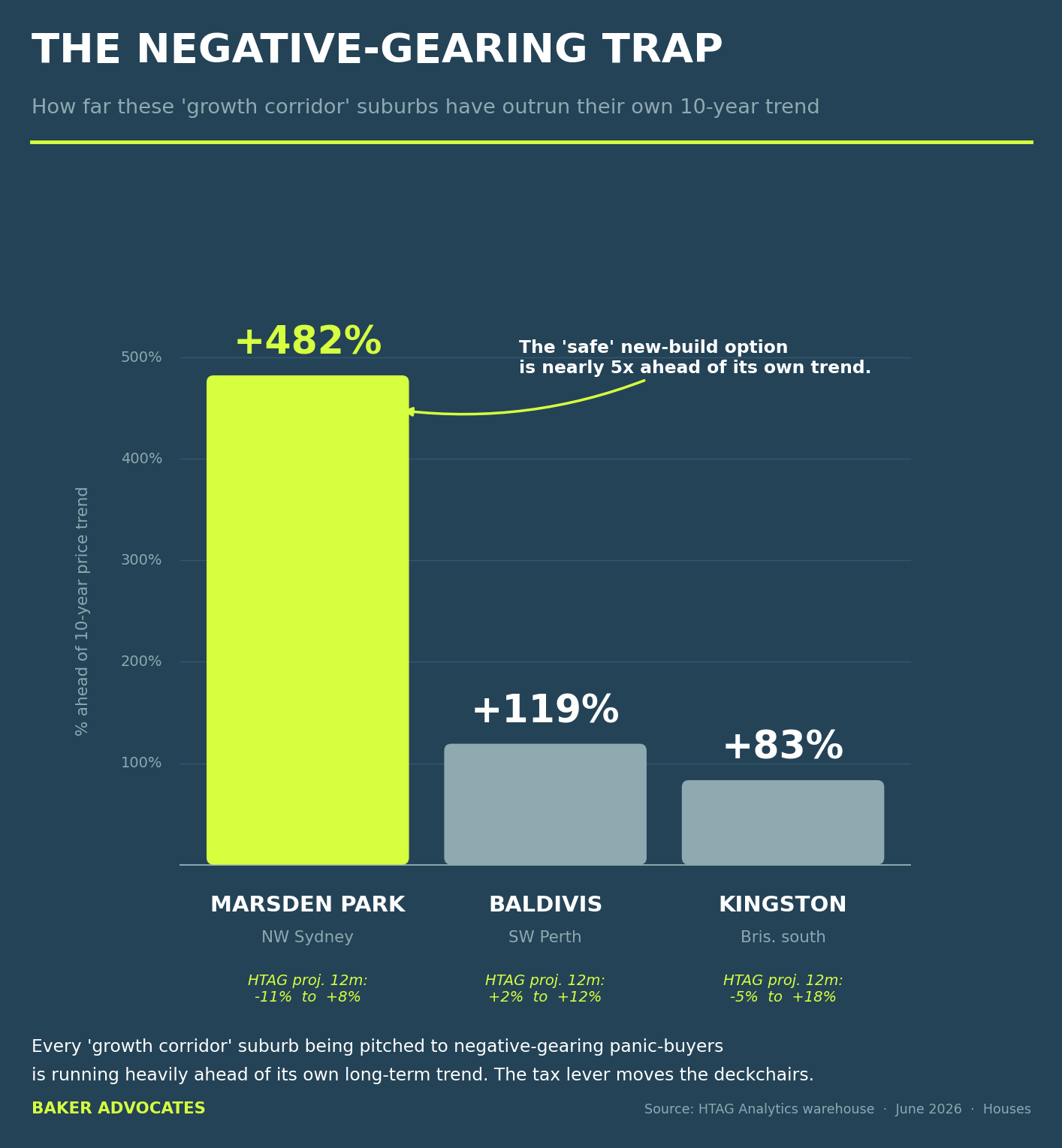

The data doesn’t lie in propertey investing. Marsden Park, Baldivis, and Kingston all ahead of their historical average.

Marsden Park (NW Sydney): 482% Ahead of Trend

10-year annualised price growth of 19.14% an extraordinary compound rate for any market, driven by a decade of land release, population inflow, and infrastructure investment. On paper, the winner.

But that same growth has pushed current pricing to 482% above the suburb's own long-term trend line. Almost five times the level HTAG's model would predict from Marsden Park's underlying fundamentals alone. The projected capital growth range for the next 12 months: -11% to +8% meaning a genuine possibility of a double-digit loss.

Marsden Park hasn't stopped being a growth story. Almost all of the story has already been priced in.

Baldivis (SW Perth): 119% Ahead of Trend

Baldivis has been one of the strongest-performing suburbs in Australia over the last three years, with annualised growth of 27.3% p.a. and a 12-month growth print of 21.07%. Perth has been the standout capital city market of 2024–2026, and Baldivis has been at the sharper end of that story.

Its GPD reading of +119% shows the suburb is currently running more than twice its own long-term expected level. The 12-month projection: +2% to +12% the only one of the three suburbs with a positive floor, but with a meaningful narrowing of runway remaining.

Kingston (Brisbane South): 83% Ahead of Trend

Brisbane's southern corridor has been a favourite of interstate investors since 2020. Kingston has delivered 20.09% annualised over five years and 18.23% in the last 12 months. Solid on the headline print.

GPD reads +83% ahead of its long-term trend. The 12-month projection: -5% to +18% a wide range that includes a real possibility of a small correction.

All three markets are still growing. None are collapsing. But all three are priced for the story that has already happened, not the story that comes next.

The Maths on Tax vs Capital Growth

Here's the calculation that should stop any investor considering a panic-buy in their tracks.

Take a $600,000 house-and-land package in an eligible new-build corridor. Standard investment structure. Reasonable annual paper loss (rental income minus interest, depreciation, expenses) of roughly $15,000 per year.

At a 30% marginal tax rate, that $15,000 paper loss saves you $4,500 in tax annually. Over five years, that's $22,500 in tax savings a meaningful number.

Now assume you buy that property into a market that returns -11% in the year following purchase (the low end of HTAG's projected range for Marsden Park). That's a $66,000 capital loss before selling costs, before opportunity cost of the deposit, before the time cost of a stalled portfolio.

Even a moderate -3% year (well within HTAG's projected range for two of the three suburbs) costs $18,000 enough to erase four years of tax savings in twelve months.

The tax lever moves the deckchairs. The cycle moves the ship. Anyone selling you a property because "the tax deadline is coming" is selling you a property, not a plan.

What This Means for Investors With a 12-Month Window

Three principles for how to think about the next 12 months.

One: don't let a tax deadline set your purchase timeline. The negative gearing changes affect the tax treatment of the asset. They don't change whether the underlying asset is a good buy. If a market isn't right for you in July 2026, the tax deadline doesn't make it right in June 2027.

Two: check GPD before you check tax. For any suburb you're considering, the first question is: how does the current price sit against the long-term trend? A suburb running 100% or more ahead of trend has already priced in a significant portion of the next decade's growth. That's compression risk, not opportunity no matter how attractive the tax treatment.

Three: match the asset to the roadmap, not the roadmap to the deadline. The whole point of a portfolio roadmap is that it tells you when, where, and how to buy to hit your goals. Tax is a downstream consideration you decide the state, then the suburb, then the asset, then the structure. Reversing that order starting with tax and working backwards is how expensive mistakes get made.

Roadmap First, Structure Second

At Baker Advocates, every new client walks through a full portfolio roadmap before we buy a single property. It's the deliberate choice we make to avoid this exact scenario a market or tax event distorting a purchase decision that should be driven by fundamentals.

The roadmap answers three questions before any property is considered:

Where are you in your investment journey, and where do you need to be in 5, 10, 15 years?

What kind of asset established vs new build, capital growth vs cashflow, house vs unit, metro vs regional matches that trajectory? This is for you and your objectives.

Which markets, right now, are best positioned to move you along that trajectory over the specific timeframe you have?

Tax structure comes at step four, not step one. It supports the decision. It doesn't drive it.

Book a Roadmap Consultation

If the negative gearing changes have you considering a purchase in the next 12 months or reconsidering a purchase you'd otherwise put off a portfolio roadmap conversation is the first step to making the decision on evidence rather than deadline pressure.

Baker Advocates is a data-led buyers agency based in Geelong, working with capital-growth investors nationally. Every roadmap is built on data plus years of on-the-ground buying experience across every mainland state.

→ Book your roadmap consultation

Troy Baker is Director and Buyers Agent at Baker Advocates. All figures in this article: HTAG Analytics warehouse, June 2026, houses. This article is general information only and does not constitute financial or tax advice. Please consult a qualified tax adviser regarding your specific circumstances.

Frequently Asked Questions

When do the negative gearing changes take effect?

The changes take effect from 1 July 2027. From that date, negative gearing on established residential properties purchased after 7:30pm on 12 May 2026 will be limited losses can only be offset against rental income or future capital gains, not against personal salary income.

Do I need to buy investment property before July 2027?

No. There's no hard deadline that forces a purchase decision. Properties bought before 7:30pm on 12 May 2026 are grandfathered under existing rules. Properties bought after that date will still be treated under the old rules until 30 June 2027. From 1 July 2027, only new builds preserve the full negative gearing treatment indefinitely. A tax deadline is a poor reason to bring forward a property purchase that isn't right on fundamentals.

Does negative gearing still apply to new builds after July 2027?

Yes. Eligible new residential dwellings remain fully negatively-gearable indefinitely, and continue to access the 50% capital gains tax discount. This is the primary reason "buy a new build" marketing has intensified since the Budget.

Should I rush a property purchase to lock in negative gearing?

Rushing a property purchase to preserve a tax benefit is a common but expensive mistake. Property is a 10-year-plus decision; negative gearing represents a small fraction of total return on a good asset. On a poor asset, it doesn't come close to offsetting capital losses. The data should drive the decision, not the tax calendar.

What is the grandfathering rule for existing property investors?

Properties owned (including those under contract awaiting settlement) at 7:30pm on 12 May 2026 are grandfathered they continue to be negatively-gearable under the old rules until sold. Selling a grandfathered property and buying a new one may trigger a change in tax treatment; investors should get specific advice before making any disposal decisions.

Which "growth corridor" suburbs are riskiest right now?

Based on HTAG data at June 2026, the north-west Sydney growth corridor (Marsden Park and comparable suburbs) is the furthest ahead of its own long-term trend, followed by Perth's outer south corridor (Baldivis and surrounds) and Brisbane's southern corridor (Kingston and Logan-area suburbs). "Ahead of trend" doesn't mean a market will fall it means the runway remaining is much narrower than the headline growth suggests.